You can be a tax resident of two countries at once — and when that happens, both of them claim the right to tax your worldwide income. That's dual tax residency, and it's a classic trap for anyone living between two places: you moved abroad but kept ties to the US, you spent too many days on both sides, or you hold a green card while living overseas. The good news is that double taxation can almost always be undone. This guide explains how the tax treaty tie-breaker works, what Form 8833 and the foreign tax credit do, and why a special clause makes life harder specifically for US citizens.

How You End Up a Resident of Two Countries

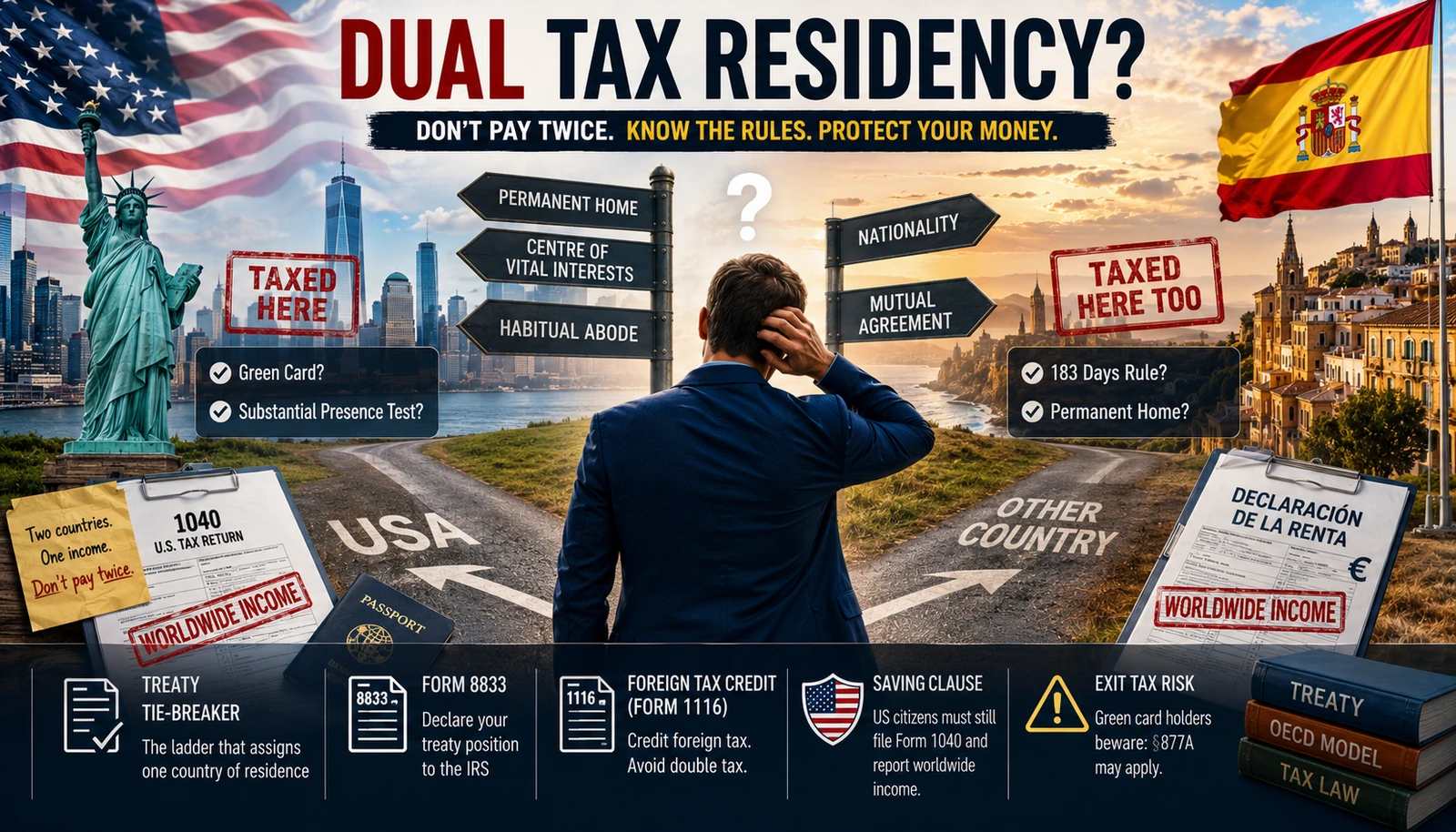

Every country sets its own residency rules. The US treats you as a resident if you hold a green card or pass the substantial presence test. Another country usually does so if you spent 183 days there or keep a permanent home there. These rules overlap easily, and you can end up a resident of both at the same time — what people search for as "dual tax resident US and Spain," or with whatever country applies to them.

The problem is that a tax resident generally pays tax on their entire worldwide income, not just local income. If two countries both treat you that way, then without protection you risk paying tax twice on the same money.

The Treaty Tie-Breaker: Assigning a Single Country of Residence

This is where the double tax treaty (DTT) comes in. Most US treaties follow the OECD Model (Article 4(2)) and contain tax treaty tie-breaker rules — a sequential ladder of tests that assigns residence to just one country. You apply them strictly in order, moving to the next step only when the current one fails to settle the question.

- Permanent home. Residence goes to the country where you have a home permanently available to you — a dwelling kept for continuous use, not a hotel room or short-term rental. If you have a permanent home in both, you move on.

- Centre of vital interests. This looks at which country your personal and economic ties are closer to: where your family lives, where you work and run a business, where your main accounts are, where you make investment decisions, your community memberships. This is the test that decides most cases.

- Habitual abode. If the centre of vital interests can't be pinned down, the tie-breaker looks at where you actually spend more time — judged by the pattern, frequency, and regularity of your stays, not a single year's day count.

- Nationality. If that still doesn't resolve it, residence goes to the country of which you're a citizen.

- Mutual agreement. If you're a citizen of both or neither, the two countries' tax authorities settle it between themselves (the mutual agreement procedure).

A point people miss: day-counting alone does not decide the tie-breaker. Days matter for domestic residency, but in the treaty ladder they only surface at the "habitual abode" rung — after permanent home and centre of vital interests.

Form 8833: Telling the IRS You're Taking a Treaty Position

Winning the tie-breaker in favour of the other country isn't enough — you have to tell the IRS. You do that with Form 8833 (Treaty-Based Return Position Disclosure). If you're claiming you're a treaty resident of the other country, you generally file Form 1040-NR with Form 8833 attached for that period.

A few things worth knowing:

- the form must name the specific treaty article, explain how the tie-breaker applies to your facts, and state the tax consequences;

- failing to make a required disclosure carries a $1,000 penalty for individuals (the IRS may waive it for reasonable cause);

- for a dual-resident tie-breaker position, the IRS flags a threshold of income items over $100,000;

- don't confuse it with Form 8840 — that one claims the closer connection exception (when you were in the US fewer than 183 days), while Form 8833 is for a treaty position.

The Saving Clause: a Catch for US Citizens

Here's where Americans have it hardest. Almost every US treaty contains a saving clause — a provision that preserves the right of the US to tax its own citizens as if the treaty didn't exist. In practice this means: a US citizen or green card holder must still file Form 1040 and report worldwide income, even if the tie-breaker makes them a treaty resident of another country. Citizenship-based taxation is a US peculiarity, and the treaty doesn't switch it off.

That doesn't mean double tax is unavoidable. It's usually erased through the foreign tax credit (Form 1116), which credits the tax you paid abroad against your US tax. For many expats this is the real answer to how to avoid double taxation with the US, while the treaty tie-breaker becomes an extra tool for specific situations.

A Special Trap for Green Card Holders

If you hold a green card and claim the tie-breaker in favour of another country, tread carefully: the IRS may read this as an intention to abandon your permanent residence. For a long-term resident, that can trigger the "exit tax" under §877A. In other words, a tax move can unexpectedly hit your immigration status. Don't do it blind in this scenario.

And Remember: States Don't Honour the Treaty

US tax treaties bind the federal government, not individual states. California, New York, and several others generally don't recognise a treaty tie-breaker position. So even after winning at the federal level, you may remain a state tax resident with a state return to file.

How to Stay Ahead of It

Dual residency almost always starts quietly — with days. You cross a threshold in one country while still resident in another, and you're in the danger zone before you realise it. And the tie-breaker, as we've seen, turns on your home, your centre of interests, and the shape of your presence — exactly the things you need to be able to document. So it pays to see, in advance, which countries you're approaching residency thresholds in and where a conflict is brewing. LumoTravel tracks your days by country and warns you about dual-residency risk early — so you can prepare your documents and your position instead of hearing about the problem after the fact from two tax authorities.

Frequently Asked Questions

What does it mean to be a tax resident of two countries?

It means each country's domestic rules treat you as its resident, and both claim the right to tax your worldwide income. A tax treaty resolves the conflict through the tie-breaker, assigning residence to one country.

How do tax treaty tie-breaker rules work?

They're a ladder of tests applied in order: permanent home → centre of vital interests → habitual abode → nationality → mutual agreement. You only drop to the next test if the current one doesn't settle it.

How do I avoid double taxation with the US?

Usually through the foreign tax credit (Form 1116), crediting foreign tax against your US tax, and/or by taking a treaty position via Form 8833. US citizens still have to file Form 1040 because of the saving clause.

What is the centre of vital interests?

It's the country your personal and economic ties are closer to — where your family lives, where you work and run a business, where your main accounts are, and where you make financial decisions. It applies when you have a permanent home in both countries or neither.

Is it risky to claim the tie-breaker if I have a green card?

Yes, it needs care. The IRS may treat it as an intention to abandon permanent residence, and for a long-term resident that can trigger an exit tax. Weigh the immigration consequences before taking that step.

This article is for general information only and is not tax advice. Treaties differ by country, IRS rules and thresholds change, and states apply their own rules. Before filing, check the current IRS instructions (irs.gov), the text of the specific treaty, and consult an international tax professional if needed.